According to Punxsutawney Phil, spring will come early this year and with it our newest report on LMS market share. We accelerated the timeline for producing this data set considering recent news that Instructure is pursuing an acquisition by a private equity firm to present factual, current data on LMS market trends. See this post for a brief review of our US methodology and this post for more information on our international methodology used for Australia, Canada, and UK.

Instructure’s Lead Widens

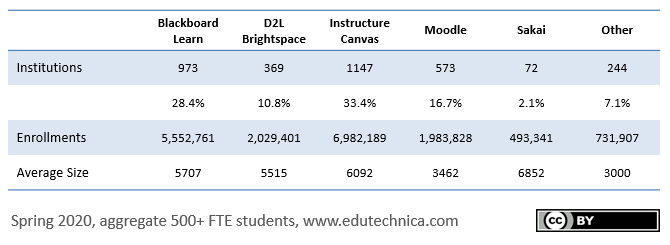

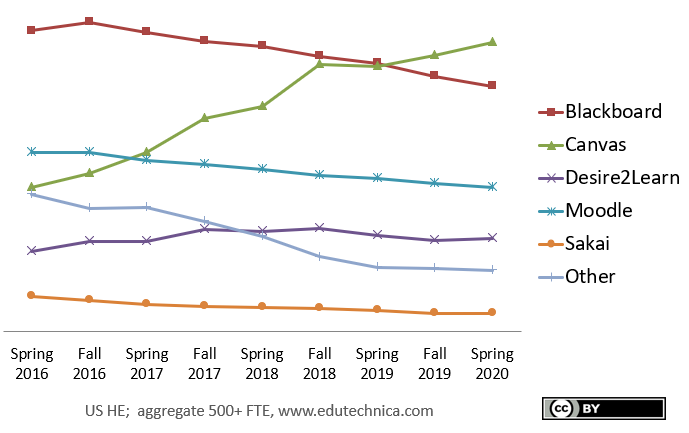

At the start of spring semester 2020, Instructure’s Canvas LMS continued to widen its lead in US higher education over top rival LMS, Blackboard Learn. D2L Brightspace also saw a slight increase, while all other LMSs saw a net decline.

Global Trends

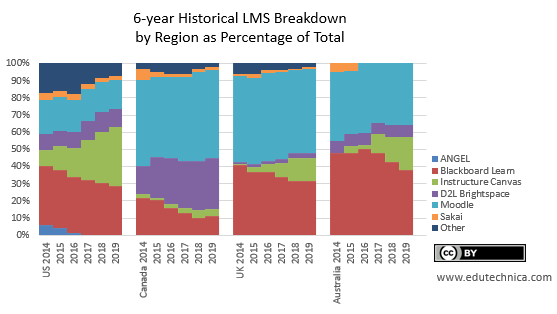

Globally, however, LMS market share has remained remarkably stable with little-to-no changes. Almost every university in Australia, Canada, and the United Kingdom continues to use the same LMS that it did last year with very few leading indicators of any impending changes. (This year’s global LMS data set, as in previous years, is available to download for free.)

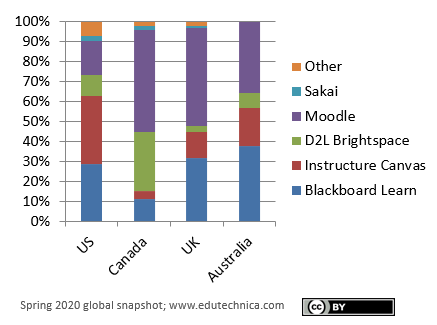

Comparing regions, Moodle continues to be the predominant LMS outside of the US with Blackboard Learn or D2L Brightspace continuing to hold the position of top commercial LMS.

Blackboard’s Positive Momentum

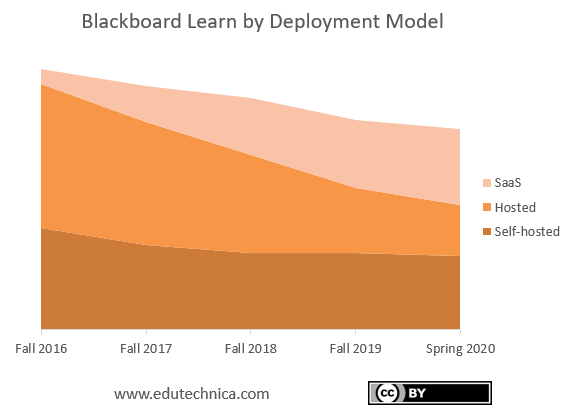

Despite gradual ongoing losses, Blackboard continues to rapidly move its user base onto its newest Learn SaaS offering. Fewer universities than ever are running older, unsupported versions of Blackboard Learn. And the newest version of Blackboard Learn is even beginning to receive positive coverage from students, who historically have been extremely critical of the company’s software.

Outlook for Instructure

Though Instructure is certainly poised for continued success, it is less well-positioned for continued growth. The market for higher-education-focused, institution-centric Learning Management System software is finite. There is a known maximum number of potential customers (the number of colleges and universities in existence), and nearly all of them currently use a LMS. Fewer institutions than ever are purchasing and supporting multiple different LMSs. And outside of the US, the data we collect indicates little-to-no appetite for switching LMSs.

As LMS software continues to evolve as a product category, there are increasingly fewer ways to differentiate one product from another. Additionally, Instructure’s competitors at this point have largely compensated for past weaknesses. Some are even beginning to argue that the LMS product category as it exists today may be becoming obsolete (1, 2, 3, 4).

In the US, financial struggles for higher education institutions continue despite a modest recovery. Demographic trends, personal financial limitations, and changes in the perceived value of a college degree are reducing the number of high school graduates immediately pursuing college as traditional students. Difficulty securing student visas has also reduced the number of international students attending US colleges and universities in recent years. These trends will have an impact on edtech software packages such as LMSs that have traditionally been licensed by the number of full-time enrolled students.

To Instructure’s credit, the company capitalized on dissatisfaction in the marketplace to secure a commanding presence that will not soon fade. At this point, however, all of Instructure’s easy wins and major system and consortium deals are almost-fully implemented with fewer and fewer schools actively considering a change in LMS. From this point onward, it is likely that each new sale will become increasingly harder to win.

There are, of course, solutions to each of the above challenges – and with every challenge comes new opportunity. We will continue to provide future data and analysis in response to developments in this space.